Table of Contents

")

Private note financing is closing more transactions than ever. Seller carry-back arrangements, non-institutional loans, and bridge financing are filling gaps that conventional lending has left open. The volume of these arrangements is accelerating.

What hasn’t kept pace is the process used to manage those notes.

That might be because most of the conversation in private lending focuses on structuring the arrangement, with less focus on what happens to the note after the transaction closes.

This post covers what’s driving the growth of private note financing, what ongoing note management requires, and how professional account servicing relieves the administrative burden for both the lender and the borrower.

Why Buyers Are Turning to Non-Institutional Lending

For 13 consecutive quarters, commercial banks have tightened small business credit, and timelines have stretched. Buyers who need to close aren’t waiting around, so private note financing has stepped into that space.

The SBA recently announced a rule that doubles the cumulative 7(a) and 504 loan limit to $10 million. This may expand funding, but it can also increase complexity and paperwork.

Seller Carry-Back Financing: When the Seller Becomes the Lender

Seller carry-back financing happens when a seller agrees to accept part of the purchase price over time rather than as a lump sum at closing. The buyer signs a promissory note, and the seller holds it. Payments flow directly from buyer to seller until the note is paid off.

It’s an arrangement that benefits both sides. Sellers attract a broader pool of buyers and can command a premium on the transaction. Buyers get flexible terms and a faster path to closing than conventional financing allows.

A growing number of transactions are using seller carry-back financing:

- The seller financing market produced $29.5 billion in volume in 2025, and over $137.8 billion in notes over the trailing five years. That’s a 4.5% increase over the prior five-year period.

- Seller-financed arrangements are now used in over 75% of transactions.

Non-Institutional Lending: When a Private Lender Originates the Loan

Seller financers aren’t the only ones holding private notes. Non-institutional and private money lenders, who originate loans outside the traditional banking system, have been filling the gap left by tighter bank credit for years.

These lenders offer financing to borrowers who can’t wait for, or don’t qualify for, conventional loans. They typically offer faster underwriting, more flexible terms, and a path to closing that doesn’t depend on a bank’s timeline.

What Happens to the Note After Closing?

Most of the conversation around private note financing focuses on structure: how to set up the promissory note, negotiate the terms, and get the transaction closed.

Very little of it focuses on what happens to the note after closing.

- Tracking every payment as it comes in.

- Calculating interest correctly each month for the exact terms of the note.

- Maintaining a running loan balance that both parties can rely on.

- Managing the lien release when the time comes.

- Issuing tax statements at the end of the year.

- Producing an accurate payoff figure when the borrower is ready to close out the note.

That responsibility defaults to the non-institutional lenders and seller-financiers.

However, many private note holders don’t plan for how long they’ll hold a note or what managing it actually involves.

And for non-institutional lenders that maintain a portfolio of notes, that administrative burden scales with every new loan.

This is where professional account servicing comes in.

Professional Account Servicing Makes the Arrangement Work

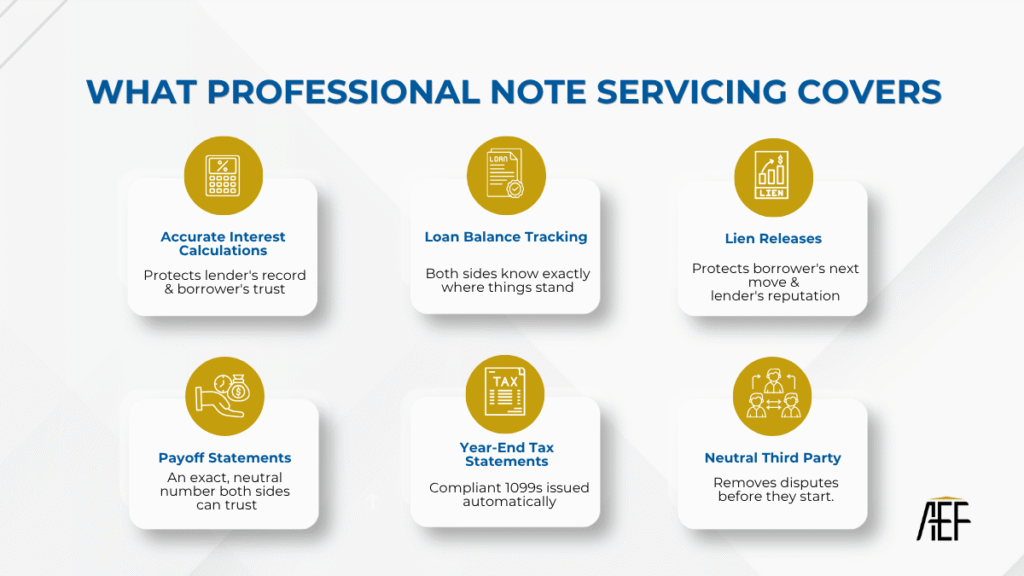

Account servicing provides ongoing, third-party management of a note from the first payment to final payoff. It covers payment collection and disbursement, principal and interest calculations, recordkeeping, tax reporting, lien releases, and payoff processing, all handled by a dedicated team, for the life of the arrangement.

It is the infrastructure that makes a private note work as intended for both the lender and the buyer.

1. Accurate interest calculations protect the lender’s record and the borrower’s trust.

Private notes often carry higher interest rates and non-standard structures: interest-only periods, balloon payments, variable terms.

- For the lender, accurate interest calculations mean accurate records. If questions arise at payoff, at refinance, or in a dispute, the numbers hold up.

- For the borrower, it means they know exactly what they owe every month without having to trust a spreadsheet maintained by the person they’re paying.

2. Ongoing loan balance tracking keeps everyone on the same page

When a payoff event approaches, like a refinance, an SBA loan coming through, or a balloon payment coming due, both sides need to know exactly where things stand.

- For the lender, a current and accurate loan balance is the foundation of every downstream action: payoff statements, lien releases, and tax reporting. Without it, nothing else is reliable.

- For the borrower, it’s a necessity, not a courtesy. When they’re ready to refinance or pay off early, they need a number they can act on.

3. Lien releases handled on time protect the borrower’s next move and the lender’s reputation.

When a note is paid off or a milestone is reached, the lien needs to be released. This step can easily be overlooked when lenders manage note servicing on their own.

- For the borrower, a lien that isn’t released on time (or a lien released with errors) can block a future sale, refinance, or title transfer.

- For the lender, a lien release problem can affect their reputation, and it creates friction at the moment the relationship should be closing cleanly.

4. Payoff statements need to be exact so both sides trust the number.

Payoff statements include the principal, accrued interest calculated to the exact day, any outstanding fees, and proper documentation for the lien release.

An informal payoff figure creates risk for both parties. If the borrower later questions the amount, or the lien wasn’t released cleanly, there’s no neutral record to rely on.

- For the borrower, this is often a significant payment. They need an accurate, independently calculated amount that fully satisfies the note.

- For the lender, an officially documented payoff statement provides a clean ending to the arrangement and the protection they need if questions come up later.

5. Compliant year-end tax statements for both sides.

At year end, the lender is required to report interest income. The borrower needs documentation for their own tax filing. In a professionally serviced arrangement, this happens automatically.

- For the lender, errors or omissions in interest income create exposure.

- For the borrower, they need an accurate 1099 to file correctly. A summary from the person they’ve been paying doesn’t meet the standard.

A professional servicer issues the correct forms to both parties and maintains the records to support them.

6. A neutral third party removes the dispute problem before it starts.

In a private note arrangement, the lender and borrower have a direct relationship and a financial one. That combination can produce disputes when records are informal, memories differ, or circumstances change.

A professional, neutral servicer maintains the record. If a question arises about payment history, interest calculations, or account status, the answer isn’t a conversation between two parties with different recollections. It’s a documented ledger from a third party that both sides can access.

- For the lender, that neutrality protects the record.

- For the borrower, it means they’re not relying on the person they’re paying to tell them where things stand. They have access to the same information, maintained by a party with no stake in the outcome.

The Work Behind the Transaction

Private note financing plays a crucial role in the current market. It is closing transactions that conventional lending can’t reach. It’s bridging gaps while SBA financing works its way through. It’s giving sellers a path to exit and buyers a path to ownership they wouldn’t otherwise have.

But the structure of the arrangement is only as strong as the infrastructure managing it.

Arizona Escrow & Financial’s account servicing department is an extension of the same role we have played in complex transactions for 50 years: a neutral party helping keep payments, balances, records, and next steps clear for everyone at the table.

Ready to hand off the administrative work?

Whether you’re holding one note or managing a portfolio, AEF’s account servicing team is here to help. Reach out to learn more.

Disclaimer: Arizona Escrow & Financial Services makes no express or implied warranty regarding the accuracy, completeness, or reliability of the information provided and assumes no responsibility for errors or omissions. The information presented is for general informational purposes only and should not be considered legal, financial, or professional advice.

Arizona Escrow & Financial Services, the Arizona Escrow logo, and www.arizonaescrow.com are trademarks or registered trademarks of Arizona Escrow & Financial Services and/or its affiliates. Unauthorized use of these trademarks is strictly prohibited.

For more information, please visit www.arizonaescrow.com or contact us directly.

Monica May-Dunn

Monica May-Dunn is the Owner, CEO, and CFO of Arizona Escrow and Financial Corp., a leading provider of business escrow services since 1976. With over 30 years of industry expertise, she has expanded AEF’s portfolio, driven record growth, and launched a leadership podcast. Recognized as one of AZRE’s “Most Influential Women in Commercial Real Estate 2024,” she is a strategic leader, mentor, and active voice in industry innovation.

Disclaimer: Arizona Escrow & Financial Services makes no express or implied warranty regarding the accuracy, completeness, or reliability of the information provided and assumes no responsibility for errors or omissions. The information presented is for general informational purposes only and should not be considered legal, financial, or professional advice.

Arizona Escrow & Financial Services, the Arizona Escrow logo, and www.arizonaescrow.com are trademarks or registered trademarks of Arizona Escrow & Financial Services and/or its affiliates. Unauthorized use of these trademarks is strictly prohibited.

For more information, please visit www.arizonaescrow.com or contact us directly.